Despite borrowing massive amounts of money, the government still needs to find ways to raise revenue to pay for new programs and spending. The current democratically controlled Congress is looking to potentially implement new social programs and a climate bill. As a way of funding these initiatives, they are considering an expansion of the Net Investment Income Tax (NIIT).

Despite borrowing massive amounts of money, the government still needs to find ways to raise revenue to pay for new programs and spending. The current democratically controlled Congress is looking to potentially implement new social programs and a climate bill. As a way of funding these initiatives, they are considering an expansion of the Net Investment Income Tax (NIIT).

The NIIT is proposed to raise revenue since it is seen as politically more palatable, given that it typically only impacts a small group of wealthier taxpayers. Critics, however, say the plan in its current form would also hurt small family businesses.

Who Pays NIIT Now?

Under the Affordable Care Act (ACA), the NIIT applied a 3.8 percent tax on investment income. Investment income includes both passive sources like dividends, capital gains, interest, royalties, and rents as well as passive business income. Under the ACA, the NIIT applied only to single taxpayers earning $200k or more and joint filers with $250k or more.

When it comes to the taxability of business income under the NIIT, because the law only captures passive business income, most owners of pass-through entities must pay the NIIT; however, active owners of S-corporations are exempt. Likewise, if someone qualifies as a real estate professional, their income is considered active and so their rental income is also exempt.

Who Would Pay Under the New Proposed Law?

The current version of the House bill makes two major changes. First, the NIIT expands to capture all business income. Essentially, S-corporation shareholders, limited partners, and pass-through entity owners that are currently exempt would be impacted.

Second, when it comes to removing the exemption on this business income, the income threshold rises from $200k to $400k for single filers and from $250k to $500k for taxpayers filing jointly. The effect of this would be to exclude most business owners from the tax, but make filing more complex for those impacted.

Under the new rules, the Tax Policy Center projects that in 2023 the tax hike would fall on those in the top 1 percent of household incomes or those making approximately $885k or more. Further, even among the top 1 percent, more than 50 percent of the tax increase would be borne by the top 0.1 percent for those making $4 million and up.

Impact No Small Businesses

Overall, about 14 percent of taxpayers report some form of business income on their federal tax returns. The amount reported, however, is usually not a material amount for most as a percentage of their income. For example, only approximately 5.5 percent of taxpayers with reported business income had this as the source of 50 percent or more of their total income. As a result, the impact will be mostly on a small percentage of small businesses. At the same time, as business income is far more variable than employment income, someone could easily fall in and out of the tax range.

Conclusion

Overall, the House bill looks to raise the threshold of where the NIIT expansion applies by the type of income it captures. We will have to wait and see if there are changes as the bill makes its way through – if it even passes at all. No matter what happens, there will certainly be tax increases of some kind.

Imagine selling slices of a large pizza. You can cut it into four even slices and charge $2 a slice. Or, you can cut it into eight even slices and charge $1 per slice. Either way, the total value of the pizza will still be $8.

Imagine selling slices of a large pizza. You can cut it into four even slices and charge $2 a slice. Or, you can cut it into eight even slices and charge $1 per slice. Either way, the total value of the pizza will still be $8. Corporate profits, according to the Bureau of Economic Analysis, grew by $20.4 billion in the final quarter of 2021, a 0.7 percent increase. For the first quarter of 2022, corporate profits fell by 2.3 percent or $66.4 billion. On an annualized basis, corporate profits fell 5.2 percent in 2022, but grew 25 percent in 2021. With the economy facing inflation, the uncertainty of the Russia/Ukraine conflict, and the world working its way out of the COVID-19 pandemic, economic uncertainty abounds. For companies, measuring margins is one way to evaluate performance and strategize ways to survive and thrive in a dynamic economy. Here are a few common margins that businesses can determine to measure their financial performance.

Corporate profits, according to the Bureau of Economic Analysis, grew by $20.4 billion in the final quarter of 2021, a 0.7 percent increase. For the first quarter of 2022, corporate profits fell by 2.3 percent or $66.4 billion. On an annualized basis, corporate profits fell 5.2 percent in 2022, but grew 25 percent in 2021. With the economy facing inflation, the uncertainty of the Russia/Ukraine conflict, and the world working its way out of the COVID-19 pandemic, economic uncertainty abounds. For companies, measuring margins is one way to evaluate performance and strategize ways to survive and thrive in a dynamic economy. Here are a few common margins that businesses can determine to measure their financial performance. Today, businesses have to grapple with vast amounts of data from different sources, including emails, mailing lists, customer orders, system logs, mobile apps, social media networks, etc. This data is crucial to businesses in various ways. When analyzed, a business can identify operational issues, personalize the customer experience and manage supply chains – all contributing to better decision-making.

Today, businesses have to grapple with vast amounts of data from different sources, including emails, mailing lists, customer orders, system logs, mobile apps, social media networks, etc. This data is crucial to businesses in various ways. When analyzed, a business can identify operational issues, personalize the customer experience and manage supply chains – all contributing to better decision-making. We’re all feeling the pain at the pump. Unless you decide to walk, bike or take public transportation, you might feel stuck. But all is not lost. Here are some fuel-efficient driving techniques that can help you save hundreds of dollars in fuel each year.

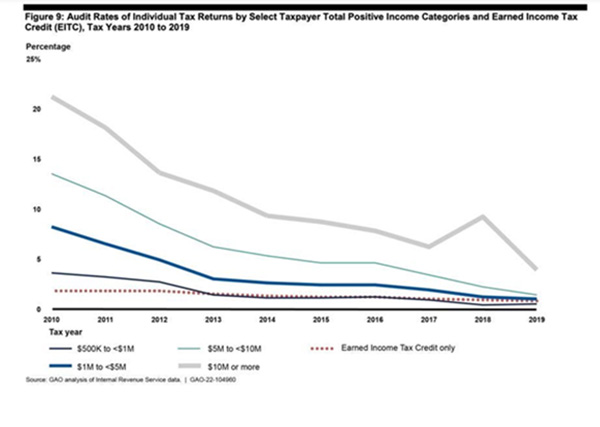

We’re all feeling the pain at the pump. Unless you decide to walk, bike or take public transportation, you might feel stuck. But all is not lost. Here are some fuel-efficient driving techniques that can help you save hundreds of dollars in fuel each year. One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into the heart of taxpayers. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into the heart of taxpayers. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

Often the first house a person buys is an affordable condominium, townhouse or older single-family dwelling, also referred to as a “starter home.” It might be small and lack features they dream about, from new appliances in the kitchen, to dual sinks in the bath, to a large yard or a garage.

Often the first house a person buys is an affordable condominium, townhouse or older single-family dwelling, also referred to as a “starter home.” It might be small and lack features they dream about, from new appliances in the kitchen, to dual sinks in the bath, to a large yard or a garage. Supreme Court Police Parity Act of 2022 (S 4160) – In response to potential threats and protests outside the homes of Supreme Court judges following a leak of their preliminary judgement on a case related to Roe vs. Wade, this bill authorizes extra security for the justices and their families. Specifically, Supreme Court justices and their families would be provided with security detail similar to that of other top government officials and families in the executive branch (e.g., the president and vice president) and legislative branch (e.g., Speaker of the House and Senate Majority Leader). This type of detail generally cannot be declined. The bill was introduced by Sen. John Cornyn (R-TX) on May 5. It passed in both the Senate and the House on June 14 and was signed into law by the president on June 16.

Supreme Court Police Parity Act of 2022 (S 4160) – In response to potential threats and protests outside the homes of Supreme Court judges following a leak of their preliminary judgement on a case related to Roe vs. Wade, this bill authorizes extra security for the justices and their families. Specifically, Supreme Court justices and their families would be provided with security detail similar to that of other top government officials and families in the executive branch (e.g., the president and vice president) and legislative branch (e.g., Speaker of the House and Senate Majority Leader). This type of detail generally cannot be declined. The bill was introduced by Sen. John Cornyn (R-TX) on May 5. It passed in both the Senate and the House on June 14 and was signed into law by the president on June 16. You love summer, don’t you? School’s out, and BBQs are on. But what you probably don’t love are those higher air conditioning bills. Here are some tried-and-true ways to help lower the cost of keeping cool.

You love summer, don’t you? School’s out, and BBQs are on. But what you probably don’t love are those higher air conditioning bills. Here are some tried-and-true ways to help lower the cost of keeping cool. Cash flow awareness is vital in running the day-to-day activities of a business. Keeping track of the inflows and outflows helps a company make better plans and decisions, such as the right time to expand. Cash flow knowledge reveals where a business is spending money and can protect business relations, among other benefits. However, tracking cash flow is a challenge for many businesses.

Cash flow awareness is vital in running the day-to-day activities of a business. Keeping track of the inflows and outflows helps a company make better plans and decisions, such as the right time to expand. Cash flow knowledge reveals where a business is spending money and can protect business relations, among other benefits. However, tracking cash flow is a challenge for many businesses.