Every year, typically right after the new year starts, the IRS formally announces key dates and deadlines for the current tax season. Recently, the IRS made the announcements for the current 2023 tax season.

To make sure the process goes as smoothly as possible, it’s best if you are aware of this tax season’s deadlines and key dates so you don’t miss a beat in working with your CPA.

Tax Season in Perspective

More than 168 million individual tax returns are expected to be submitted to the IRS in 2023, covering the 2022 tax year. The last three years saw delays and snafus, largely impacted by the pandemic. This year, the IRS assures taxpayers it is taking measures to streamline filings.

Under the recently passed Inflation Reduction Act, the IRS hired thousands of customer service representatives. They will be on call to assist with answering questions via the IRA taxpayer helpline. The helpline number is: 1-800-829-1040; additionally, online tools and resources can be found on the IRS website.

The IRS also provides other free assistance services, such as its Volunteer Income Tax Assistance and Tax Counseling for the Elderly for qualified individuals.

Important Dates for the 2023 Tax Filing Season

IRS Free Filing Opens for the season – Jan. 13

Opening 10 days earlier than the regular official start of the season, the IRS free file program offers taxpayers making less than $73,000 in 2022 to file free of charge using online tax software.

Estimated Tax Payments for the 2022 tax year 4th quarter – Jan. 17

First day the IRS starts accepting and processing 2023 tax season (2022 fiscal year) individual tax returns – Jan. 23

Earned Income Tax Credit (EITC) Awareness Day – Jan. 27

This day is designed to raise awareness of the EITC availability to low- and moderate-income workers and families who may qualify but are unaware.

Due date for 2022 tax returns to be filed or extension requested, tax due to be paid – April 18

This deadline is an additional three days beyond the typical deadline of April 15, granted due to the Emancipation Day holiday in Washington, D.C., and the way the weekend falls.

Note that refunds are expected to be issued in 21 days or less (if using the direct deposit option and filing electronically).

Due date for 2022 individual tax returns put on extension – Oct. 16

Gather Your Important Documents

Keeping these dates and deadlines in mind, make sure you organize and gather all your tax records and documents as you receive them electronically or in the mail. This will make it faster and easier to work with your tax professional.

Conclusion

Keep in mind the above dates as you organize and prepare for the 2023 tax season. Doing so will make your life much easier and less stressful when it comes to taxes.

Key Deadlines and Changes for the 2023 Tax Season

February 1, 2023 · Blog, News, Tax and Financial News

⏱ 3 min read

Every year, typically right after the new year starts, the IRS formally announces key dates and deadlines for the current tax season. Recently, the IRS made the announcements for the current 2023 tax season.

To make sure the process goes as smoothly as possible, it’s best if you are aware of this tax season’s deadlines and key dates so you don’t miss a beat in working with your CPA.

Tax Season in Perspective

More than 168 million individual tax returns are expected to be submitted to the IRS in 2023, covering the 2022 tax year. The last three years saw delays and snafus, largely impacted by the pandemic. This year, the IRS assures taxpayers it is taking measures to streamline filings.

Under the recently passed Inflation Reduction Act, the IRS hired thousands of customer service representatives. They will be on call to assist with answering questions via the IRA taxpayer helpline. The helpline number is: 1-800-829-1040; additionally, online tools and resources can be found on the IRS website.

The IRS also provides other free assistance services, such as its Volunteer Income Tax Assistance and Tax Counseling for the Elderly for qualified individuals.

Important Dates for the 2023 Tax Filing Season

IRS Free Filing Opens for the season – Jan. 13

Opening 10 days earlier than the regular official start of the season, the IRS free file program offers taxpayers making less than $73,000 in 2022 to file free of charge using online tax software.

Estimated Tax Payments for the 2022 tax year 4th quarter – Jan. 17

First day the IRS starts accepting and processing 2023 tax season (2022 fiscal year) individual tax returns – Jan. 23

Earned Income Tax Credit (EITC) Awareness Day – Jan. 27

This day is designed to raise awareness of the EITC availability to low- and moderate-income workers and families who may qualify but are unaware.

Due date for 2022 tax returns to be filed or extension requested, tax due to be paid – April 18

This deadline is an additional three days beyond the typical deadline of April 15, granted due to the Emancipation Day holiday in Washington, D.C., and the way the weekend falls.

Note that refunds are expected to be issued in 21 days or less (if using the direct deposit option and filing electronically).

Due date for 2022 individual tax returns put on extension – Oct. 16

Gather Your Important Documents

Keeping these dates and deadlines in mind, make sure you organize and gather all your tax records and documents as you receive them electronically or in the mail. This will make it faster and easier to work with your tax professional.

Conclusion

Keep in mind the above dates as you organize and prepare for the 2023 tax season. Doing so will make your life much easier and less stressful when it comes to taxes.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

According to the IRS, ignorance of tax rules and regulations is no excuse. Therefore, it’s essential to use an experienced tax preparer to assist in filing your taxes. The tax code is complex and only gets more complicated as time goes on, making it almost impossible to ensure they are filing correctly without the help of a CPA, EA, or Tax Professional.

Moreover, the penalty for making what could be deemed an innocent mistake can cost a taxpayer a significant sum. What is worse yet is that defending yourself against the IRS is a costly endeavor in terms of both time and money. Part of the problem is that taxpayers often do not have the option of making an appeal directly to the tax court and instead need to first pay the IRS and then challenge it in either District Court or the Court of Claims. Stated plainly, the average taxpayer simply can not afford to fight the IRS in tax court.

In the remainder of this article, we will look at two main areas that tend to be problematic for taxpayers: first assorted penalties for misfiling and mistake, and second obscure international form.

Miscellaneous Mishaps and Mistakes

Taxpayers can get caught up in “gotcha” type situations where they inadvertently make a mistake in the type, accuracy or timing of the filings. Here is a checklist of some of the most common issues in which taxpayers typically make unintentional errors that will not be forgiven by the IRS.

Filing late and paying short: Filing a return late and underpaying the tax owed each carry separate penalties. Together, these penalties can add up to 47.5 percent of the original tax owed in a worst-case scenario.

Careless Filing Details: If you make a mistake in filing your return and it results in tax liability in your favor, you can owe a penalty of 20 percent of the under-reported taxes. In the case of faulty appraisals for items such as donated property, the penalty can double up to 40 percent.

Writing Bad Checks: Technically, it does not matter if it is a physical check or another payment method, but if a taxpayer’s payment to the IRS is declined, the IRS will charge an additional 2 percent penalty.

Missing Checklists: Failure to file the two-page “due diligence” checklist before claiming certain credits, such as earned income or college credits, can result in a fine of $545 per credit.

Obscure International Forms

Many compliance-related rules related to international investments and banking activities were originally created to put a stop to drug dealers, terrorists, and flagrant tax cheats. Unfortunately, the regulations are still in force but apply to increasingly more taxpayers as the threshold amounts have not increased yet more U.S. citizens are working, living, or retiring abroad. Moreover, the penalties can be severe. In this section, we will look at some of the most obscure and serious foreign tax compliance issues.

Passive Foreign Investments: If you own mutual fund shares incorporated abroad, you must file Form 8621.

Personal Holding Companies: If you create a corporation to hold a foreign property, you will need to file Form 5471 for a Controlled Foreign Corporation.

FBAR: If you have $10,000 or more in any combination of international bank and brokerage accounts at any single point in the year, you need to file the FBAR form electronically. Note the trigger here is that the bank or brokerage is outside the United States. If you hold securities of foreign companies or foreign currencies with a U.S. institution, the reporting is not required.

Fatca Disclosures: Facta disclosures were created to combat money laundering, covering all manner of foreign financial assets, including insurance and retirement assets. It can overlap with the FBAR requirements, but the additional reporting here is triggered by higher thresholds starting at $50,000 in assets for single U.S. residents and up to $400,000 for couples residing abroad and filing joint returns.

Conclusion

Remember that ignorance of the tax law is no excuse, especially in the eyes of the IRS. It does not matter if a mistake you make is truly innocent; there is still a good chance that you will end up with unpleasant fines and penalties and, in the worst case, a big mess. It is best to be timely and diligent in your filings, and if your situation is anything short of vanilla, to engage a competent tax professional. More on whos responsible can usually be found in your annual engagement letter from your tax professional.

The IRS Versus the Taxpayer

January 1, 2023 · Blog, News, Tax and Financial News

⏱ 4 min read

According to the IRS, ignorance of tax rules and regulations is no excuse. Therefore, it’s essential to use an experienced tax preparer to assist in filing your taxes. The tax code is complex and only gets more complicated as time goes on, making it almost impossible to ensure they are filing correctly without the help of a CPA, EA, or Tax Professional.

Moreover, the penalty for making what could be deemed an innocent mistake can cost a taxpayer a significant sum. What is worse yet is that defending yourself against the IRS is a costly endeavor in terms of both time and money. Part of the problem is that taxpayers often do not have the option of making an appeal directly to the tax court and instead need to first pay the IRS and then challenge it in either District Court or the Court of Claims. Stated plainly, the average taxpayer simply can not afford to fight the IRS in tax court.

In the remainder of this article, we will look at two main areas that tend to be problematic for taxpayers: first assorted penalties for misfiling and mistake, and second obscure international form.

Miscellaneous Mishaps and Mistakes

Taxpayers can get caught up in “gotcha” type situations where they inadvertently make a mistake in the type, accuracy or timing of the filings. Here is a checklist of some of the most common issues in which taxpayers typically make unintentional errors that will not be forgiven by the IRS.

Filing late and paying short: Filing a return late and underpaying the tax owed each carry separate penalties. Together, these penalties can add up to 47.5 percent of the original tax owed in a worst-case scenario.

Careless Filing Details: If you make a mistake in filing your return and it results in tax liability in your favor, you can owe a penalty of 20 percent of the under-reported taxes. In the case of faulty appraisals for items such as donated property, the penalty can double up to 40 percent.

Writing Bad Checks: Technically, it does not matter if it is a physical check or another payment method, but if a taxpayer’s payment to the IRS is declined, the IRS will charge an additional 2 percent penalty.

Missing Checklists: Failure to file the two-page “due diligence” checklist before claiming certain credits, such as earned income or college credits, can result in a fine of $545 per credit.

Obscure International Forms

Many compliance-related rules related to international investments and banking activities were originally created to put a stop to drug dealers, terrorists, and flagrant tax cheats. Unfortunately, the regulations are still in force but apply to increasingly more taxpayers as the threshold amounts have not increased yet more U.S. citizens are working, living, or retiring abroad. Moreover, the penalties can be severe. In this section, we will look at some of the most obscure and serious foreign tax compliance issues.

Passive Foreign Investments: If you own mutual fund shares incorporated abroad, you must file Form 8621.

Personal Holding Companies: If you create a corporation to hold a foreign property, you will need to file Form 5471 for a Controlled Foreign Corporation.

FBAR: If you have $10,000 or more in any combination of international bank and brokerage accounts at any single point in the year, you need to file the FBAR form electronically. Note the trigger here is that the bank or brokerage is outside the United States. If you hold securities of foreign companies or foreign currencies with a U.S. institution, the reporting is not required.

Fatca Disclosures: Facta disclosures were created to combat money laundering, covering all manner of foreign financial assets, including insurance and retirement assets. It can overlap with the FBAR requirements, but the additional reporting here is triggered by higher thresholds starting at $50,000 in assets for single U.S. residents and up to $400,000 for couples residing abroad and filing joint returns.

Conclusion

Remember that ignorance of the tax law is no excuse, especially in the eyes of the IRS. It does not matter if a mistake you make is truly innocent; there is still a good chance that you will end up with unpleasant fines and penalties and, in the worst case, a big mess. It is best to be timely and diligent in your filings, and if your situation is anything short of vanilla, to engage a competent tax professional. More on whos responsible can usually be found in your annual engagement letter from your tax professional.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

Now is the time of year to do everything you can to minimize taxes and maximize your financial health with proper year-end planning. In this article, we’ll look at several actions to consider taking before the end of 2022.

Thoughtfully Harvest Losses and Gains Before Year-End

Tax loss harvesting by selling securities at a loss to offset capital gains is a classic year-end planning strategy. Just make sure not to violate the wash sale rules. This means you can’t buy back the same security or a substantially identical one within 30 days of the sale.

Reinvest Capital Gains into Opportunity Zones

Another way to offset capital gains is to reinvest those gains into a qualified opportunity fund (QOF). To be eligible, you must make the investment within 180 days of the sale of the asset-bearing gains. QOF investments allow you to defer the recognition of the capital gains tax on the original investment. The details and exact rules can be tricky, so it’s best to check with your tax advisor before making this type of transaction.

Consider Installment Sales Where Applicable

When a taxpayer sells a private asset such as real estate, a business, or private equity in exchange for a series of payments over multiple years through a promissory note, this can constitute an installment sale. Installment sales are generally taxed, with each payment representing a portion of the proceeds; return of basis, interest, and gain are recognized over the life of the note.

There are situations in which installment sales can be structured so that gains are not recognized until principal payments are recouped. If you are considering selling an asset via an installment sale this year-end or next, consult with your tax advisor to determine if it’s possible to structure the sale to defer gains.

Funding Retirement

If you can contribute to a retirement account, now is the time to see if you need to make additional contributions or top-up to the full amount allowable. As you review your situation, keep in mind the annual maximum contribution limits for 2022.

IRAs – $6,000. If you are 50 or older, it’s $7,000.

401(k)s/403(b)s — $20,500. If you are 50 or older, it’s $27,000

Also, converting assets from a traditional IRA to a Roth IRA may be a smart move if: you believe your tax rate will be higher in the future; you can afford to pay the taxes now with spare cash; and you don’t plan to leave the IRA assets to charity.

Take Your Required Minimum Distributions

The annual deadline to take required minimum distributions (RMD) from your own or inherited retirement accounts is Dec. 31, 2022. It’s important to take RMDs because there is a 50 percent penalty on amounts not distributed. The amount needed to be taken were determined on Dec. 31, 2021, even though the value of the investment has likely fluctuated significantly since that time. RMDs are based on a calculation of age and amount of assets. There are online calculators to help you figure out the amount you need to take.

Giving to Charity

Some taxpayers believe that the deduction for charitable donations is no longer applicable to them since it can be hard to make donations large enough to exceed the standard deduction. One strategy to overcome this challenge is to cluster your donations. Instead of making equal gifts every year, consider making more substantial gifts all in one year instead.

When it comes to making donations around year-end, it’s important to understand the rules on timing and when a gift is effectively deemed given for tax purposes. Here are the basic rules on timing of charitable donations.

To give to charity by check => the date the check is mailed

Gifts of stock certificates => when the transfer occurs, according to the issuer’s records

Gifts of stocks by electronic transfer => when the stock is received, according to the issuer’s records

Gifts by credit card => date the charge is made

Conclusion

As we enter the final part of the year, now is the time to take stock of your financial and tax situation to see if there are any moves you can make to minimize your 2022 tax liabilities and maximize your wealth.

The 2022 Tax Guide

December 1, 2022 · Blog, News, Tax and Financial News

⏱ 4 min read

Now is the time of year to do everything you can to minimize taxes and maximize your financial health with proper year-end planning. In this article, we’ll look at several actions to consider taking before the end of 2022.

Thoughtfully Harvest Losses and Gains Before Year-End

Tax loss harvesting by selling securities at a loss to offset capital gains is a classic year-end planning strategy. Just make sure not to violate the wash sale rules. This means you can’t buy back the same security or a substantially identical one within 30 days of the sale.

Reinvest Capital Gains into Opportunity Zones

Another way to offset capital gains is to reinvest those gains into a qualified opportunity fund (QOF). To be eligible, you must make the investment within 180 days of the sale of the asset-bearing gains. QOF investments allow you to defer the recognition of the capital gains tax on the original investment. The details and exact rules can be tricky, so it’s best to check with your tax advisor before making this type of transaction.

Consider Installment Sales Where Applicable

When a taxpayer sells a private asset such as real estate, a business, or private equity in exchange for a series of payments over multiple years through a promissory note, this can constitute an installment sale. Installment sales are generally taxed, with each payment representing a portion of the proceeds; return of basis, interest, and gain are recognized over the life of the note.

There are situations in which installment sales can be structured so that gains are not recognized until principal payments are recouped. If you are considering selling an asset via an installment sale this year-end or next, consult with your tax advisor to determine if it’s possible to structure the sale to defer gains.

Funding Retirement

If you can contribute to a retirement account, now is the time to see if you need to make additional contributions or top-up to the full amount allowable. As you review your situation, keep in mind the annual maximum contribution limits for 2022.

IRAs – $6,000. If you are 50 or older, it’s $7,000.

401(k)s/403(b)s — $20,500. If you are 50 or older, it’s $27,000

Also, converting assets from a traditional IRA to a Roth IRA may be a smart move if: you believe your tax rate will be higher in the future; you can afford to pay the taxes now with spare cash; and you don’t plan to leave the IRA assets to charity.

Take Your Required Minimum Distributions

The annual deadline to take required minimum distributions (RMD) from your own or inherited retirement accounts is Dec. 31, 2022. It’s important to take RMDs because there is a 50 percent penalty on amounts not distributed. The amount needed to be taken were determined on Dec. 31, 2021, even though the value of the investment has likely fluctuated significantly since that time. RMDs are based on a calculation of age and amount of assets. There are online calculators to help you figure out the amount you need to take.

Giving to Charity

Some taxpayers believe that the deduction for charitable donations is no longer applicable to them since it can be hard to make donations large enough to exceed the standard deduction. One strategy to overcome this challenge is to cluster your donations. Instead of making equal gifts every year, consider making more substantial gifts all in one year instead.

When it comes to making donations around year-end, it’s important to understand the rules on timing and when a gift is effectively deemed given for tax purposes. Here are the basic rules on timing of charitable donations.

To give to charity by check => the date the check is mailed

Gifts of stock certificates => when the transfer occurs, according to the issuer’s records

Gifts of stocks by electronic transfer => when the stock is received, according to the issuer’s records

Gifts by credit card => date the charge is made

Conclusion

As we enter the final part of the year, now is the time to take stock of your financial and tax situation to see if there are any moves you can make to minimize your 2022 tax liabilities and maximize your wealth.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

The recent hurricane Ian impacted much of the southeast United States. As a result, it is good to know the general tax rules related to disaster victims. Below, we look at several tax topics for disaster area victims.

1. Tax Returns and Filings

Q: I am a disaster area victim and needed to move from my home. I might not be back for a long time or even at all. Which address should I use on my tax return?

A: A taxpayer should always use their current address in filing a tax return. In the situation where you move after filing your return, you need to update your address with the IRS. You can do this either by filing form 8822 or calling the IRS Disaster Hotline at 866-562-5227.

Q: I filed an extension for my form 1040, giving me until Oct. 15 to file. Are there any further extensions available?

A: Taxpayers who already filed for an extension until Oct. 15 and live in a federally declared disaster area of the recent hurricanes receive an automatic extension due date of Dec. 31.

2. Payments

Q: I have a balance due on my 2021 tax return and am currently accruing interest on it. Is there any relief for disaster victims on interest charges?

A: No, the IRS is not giving any forbearance or cancellation of interest on tax balance liabilities. The IRS is, however, willing to waive late payment penalties when the taxpayer can prove the reason they are late is caused by issues related to the disaster.

3. Property and Casualty Loss

Q: During a recent disaster, we lost electricity, and all the food in my refrigerator and freezers spoiled, and I had to throw it away. My homeowners’ insurance reimbursed me, and it was for more than the food cost me. Do I have to report any income on the amount over my food costs?

A: No. The tax code makes a distinction between scheduled property and general reimbursements. For unscheduled property (general reimbursements), the taxpayer does not need to recognize income for reimbursements on personal property, even if it was more than the cost of the lost property.

Q: I need to prove the reasonable value (FMV) of my home. Am I allowed to use property tax assessments to substantiate the FMV of my home?

A: No, the only way a taxpayer can establish the FMV of a property is either with an appraisal by a credentialed appraiser or using the cost of repairs method.

4. Sale of Home

Q: My primary residence was destroyed, and the cause was deemed to be a federally declared disaster. After clearing the lot, I sold the land alone for a gain. Do I have to pay taxes on the gain or is there an exclusion since it is where my primary residence used to be?

A: Selling a vacant lot does not qualify for the exemption on gains from primary residences. The exception to this rule is if the land previously had the taxpayer’s main residence on it. In this case, if the taxpayer would have qualified for the main residence exemption before the disaster, the gain on the sale of the vacant land would be exempt here as well.

5. Expenses

Q: I worked in a federally declared disaster area and had to move for my job at my own expense. Can I deduct my travel and related expenses?

A: The answer depends on whether or not the move is expected to last for more than one year. If you expect the move to be temporary, defined as less than one year, then there is no change in your tax home. In this case, you can deduct travel and related expenses to get you both to and back from your temporary work assignment. If the move is long-term, defined as more than one year, then the expenses are not deductible, regardless of whether your employer reimbursed you.

Tax Planning Guide for Disaster Area Victims

November 1, 2022 · Blog, News, Tax and Financial News

⏱ 4 min read

The recent hurricane Ian impacted much of the southeast United States. As a result, it is good to know the general tax rules related to disaster victims. Below, we look at several tax topics for disaster area victims.

1. Tax Returns and Filings

Q: I am a disaster area victim and needed to move from my home. I might not be back for a long time or even at all. Which address should I use on my tax return?

A: A taxpayer should always use their current address in filing a tax return. In the situation where you move after filing your return, you need to update your address with the IRS. You can do this either by filing form 8822 or calling the IRS Disaster Hotline at 866-562-5227.

Q: I filed an extension for my form 1040, giving me until Oct. 15 to file. Are there any further extensions available?

A: Taxpayers who already filed for an extension until Oct. 15 and live in a federally declared disaster area of the recent hurricanes receive an automatic extension due date of Dec. 31.

2. Payments

Q: I have a balance due on my 2021 tax return and am currently accruing interest on it. Is there any relief for disaster victims on interest charges?

A: No, the IRS is not giving any forbearance or cancellation of interest on tax balance liabilities. The IRS is, however, willing to waive late payment penalties when the taxpayer can prove the reason they are late is caused by issues related to the disaster.

3. Property and Casualty Loss

Q: During a recent disaster, we lost electricity, and all the food in my refrigerator and freezers spoiled, and I had to throw it away. My homeowners’ insurance reimbursed me, and it was for more than the food cost me. Do I have to report any income on the amount over my food costs?

A: No. The tax code makes a distinction between scheduled property and general reimbursements. For unscheduled property (general reimbursements), the taxpayer does not need to recognize income for reimbursements on personal property, even if it was more than the cost of the lost property.

Q: I need to prove the reasonable value (FMV) of my home. Am I allowed to use property tax assessments to substantiate the FMV of my home?

A: No, the only way a taxpayer can establish the FMV of a property is either with an appraisal by a credentialed appraiser or using the cost of repairs method.

4. Sale of Home

Q: My primary residence was destroyed, and the cause was deemed to be a federally declared disaster. After clearing the lot, I sold the land alone for a gain. Do I have to pay taxes on the gain or is there an exclusion since it is where my primary residence used to be?

A: Selling a vacant lot does not qualify for the exemption on gains from primary residences. The exception to this rule is if the land previously had the taxpayer’s main residence on it. In this case, if the taxpayer would have qualified for the main residence exemption before the disaster, the gain on the sale of the vacant land would be exempt here as well.

5. Expenses

Q: I worked in a federally declared disaster area and had to move for my job at my own expense. Can I deduct my travel and related expenses?

A: The answer depends on whether or not the move is expected to last for more than one year. If you expect the move to be temporary, defined as less than one year, then there is no change in your tax home. In this case, you can deduct travel and related expenses to get you both to and back from your temporary work assignment. If the move is long-term, defined as more than one year, then the expenses are not deductible, regardless of whether your employer reimbursed you.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

It is all about how much you keep after taxes – not what you earn from your job, a business, or investments. While it is always great to see fabulous investment gains, the only financial metric that really matters is what is in your bank account at the end of the day. One of the ways you can influence this is by minimizing the taxes you pay on your investments.

Unfortunately, many people do not think about how taxes impact their investment returns until near the end of the year; however, you should act all year round. Taking part in investment tax planning throughout the year will give you opportunities to keep more of what you earn. Here are some rules and strategies to keep in mind.

Know When to Take Your Losses

Psychologically, many investors are averse to taking losses, holding out to “make their money back.” Instead of emotion, logic and investment acumen needs to be applied here. If an investment does not have a fundamental reason to turn around, then you are better off selling it and taking a tax loss.

Losses reduce taxes on either your capital gains for the year or, when losses exceed gains, up to $3,000 on other income. Excess losses can be carried forward to future years. Plus, you will have the proceeds to reinvest in something more likely to produce a return.

Let Winners Run

Unlike long-term capital gains, short-term capital gains are taxed as ordinary income. This means your marginal income tax rate (the highest rate applied to you) can impact your investment gains.

While you should not let the tax tail wag the investment dog, ideally you want to hold a winning investment for at least a year and a day to benefit from long-term capital gains tax treatment. This means you will pay only a 20 percent maximum tax versus whatever your marginal rate is.

As with losses, the fundamentals of the investment are key. Therefore you should not sell a holding if you think the gains are at risk just to save on taxes. If you believe in the investment for the long term, then holding out for preferred capital gains treatment can be a clever idea.

Give the Gift of Appreciation

Making charitable donations you would not otherwise give is generally not a viable tax strategy. However, if you are already charitably inclined then consider donating stock or mutual funds instead of cash.

When you donate property such as stocks, your charitable deduction is based on the fair market value of the asset on the date of the gift. It is much better to do this than donate cash.

For example, if you have a stock you purchased for $35 and it is now worth $135, when you donate it you will receive a charitable deduction of $135. If you were to sell the stock first, you would have to pay tax on the $100 gains and then have only $103 to donate in cash – assuming you are in the 32 percent tax bracket. The only winner in this situation is the IRS; both you and the charity lose. This is because the charity is excluded from paying capital gains taxes on the appreciation that occurred while you owned the asset.

Hold Until You Die

This strategy does not benefit you directly, but rather your heirs. When someone inherits an asset such as real estate, stocks, bonds, mutual funds, etc., the cost basis of the asset is reset to the fair market value at the date of death.

This means that if you have stock in company XYZ that you bought for $50 and now it is worth $500, you would pay tax on the gain of $450 per share. However, your heir would pay $0 if he sold it on the day you died. If your heir continues to hold the stock, the benefit still applies as his cost basis in the stock of XYZ would reset to $500, so he will pay taxes only on gains over that amount.

Conclusion

While you should never cheat on your taxes or do anything unethical, it is foolish to pay any more than legally necessary to the IRS. Engage in investment tax planning year-round and you may see better after-tax returns and more money in your bank account.

How to Increase After-Tax Returns on Investments

October 1, 2022 · Blog, News, Tax and Financial News

⏱ 4 min read

It is all about how much you keep after taxes – not what you earn from your job, a business, or investments. While it is always great to see fabulous investment gains, the only financial metric that really matters is what is in your bank account at the end of the day. One of the ways you can influence this is by minimizing the taxes you pay on your investments.

Unfortunately, many people do not think about how taxes impact their investment returns until near the end of the year; however, you should act all year round. Taking part in investment tax planning throughout the year will give you opportunities to keep more of what you earn. Here are some rules and strategies to keep in mind.

Know When to Take Your Losses

Psychologically, many investors are averse to taking losses, holding out to “make their money back.” Instead of emotion, logic and investment acumen needs to be applied here. If an investment does not have a fundamental reason to turn around, then you are better off selling it and taking a tax loss.

Losses reduce taxes on either your capital gains for the year or, when losses exceed gains, up to $3,000 on other income. Excess losses can be carried forward to future years. Plus, you will have the proceeds to reinvest in something more likely to produce a return.

Let Winners Run

Unlike long-term capital gains, short-term capital gains are taxed as ordinary income. This means your marginal income tax rate (the highest rate applied to you) can impact your investment gains.

While you should not let the tax tail wag the investment dog, ideally you want to hold a winning investment for at least a year and a day to benefit from long-term capital gains tax treatment. This means you will pay only a 20 percent maximum tax versus whatever your marginal rate is.

As with losses, the fundamentals of the investment are key. Therefore you should not sell a holding if you think the gains are at risk just to save on taxes. If you believe in the investment for the long term, then holding out for preferred capital gains treatment can be a clever idea.

Give the Gift of Appreciation

Making charitable donations you would not otherwise give is generally not a viable tax strategy. However, if you are already charitably inclined then consider donating stock or mutual funds instead of cash.

When you donate property such as stocks, your charitable deduction is based on the fair market value of the asset on the date of the gift. It is much better to do this than donate cash.

For example, if you have a stock you purchased for $35 and it is now worth $135, when you donate it you will receive a charitable deduction of $135. If you were to sell the stock first, you would have to pay tax on the $100 gains and then have only $103 to donate in cash – assuming you are in the 32 percent tax bracket. The only winner in this situation is the IRS; both you and the charity lose. This is because the charity is excluded from paying capital gains taxes on the appreciation that occurred while you owned the asset.

Hold Until You Die

This strategy does not benefit you directly, but rather your heirs. When someone inherits an asset such as real estate, stocks, bonds, mutual funds, etc., the cost basis of the asset is reset to the fair market value at the date of death.

This means that if you have stock in company XYZ that you bought for $50 and now it is worth $500, you would pay tax on the gain of $450 per share. However, your heir would pay $0 if he sold it on the day you died. If your heir continues to hold the stock, the benefit still applies as his cost basis in the stock of XYZ would reset to $500, so he will pay taxes only on gains over that amount.

Conclusion

While you should never cheat on your taxes or do anything unethical, it is foolish to pay any more than legally necessary to the IRS. Engage in investment tax planning year-round and you may see better after-tax returns and more money in your bank account.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

One highlight of the recently passed Inflation Reduction Act of 2022 (IRA; HR 5376) includes modifications to what is more commonly referred to as EV credits. Specifically, Section 30D of the Act is where the most important modifications are, and where the present tax credit for electric vehicles is spelled out in the U.S. Code. There is also new stimulus for previously owned electric vehicles, industrial vehicles and “alternative fuel refueling property.”

According to the Joint Committee on Taxation’s estimates, in lieu of what was previously known as the credit for plug-in electric vehicles, there is now a new clean vehicle credit. It is expected to be worth $7.5 billion over the next decade. Other noteworthy tax credits include $1.7 billion for “alternative fuel refueling property,” $1.3 billion available for buying a previously owned qualified plug-in EV, and $3.6 billion in tax credits for qualified commercial clean vehicles.

How the IRA Changes Section 30D and EV Tax Credits

For eligible, new clean vehicles, purchasers may receive $7,500 in federal tax credits and $4,000 for similarly used vehicles. It is important to note that taxpayers who purchase such vehicles are eligible for this tax credit if their modified adjusted gross income (MAGI) during the current or preceding tax year is no greater than $300,000 for joint filers; $225,000 for heads of household; and $150,000 for single filers. It is also limited to pickup trucks, vans, and sport utility vehicles up to a MSRP of $80,000. All other vehicles costing up to $55,000 are similarly eligible.

Critical Mineral Standards

Another important qualification for this tax credit is if the vehicle’s battery has a minimum threshold of critical minerals and if it has been processed in the required geographies. Section 30D(e) requires progressively increasing percentages of critical minerals either processed or extracted in the United States or another country the U.S. has an existing free-trade agreement with. If the stated percentages are recycled in North America, a vehicle’s battery components may also qualify for the tax credit.

Once guidance is issued by the U.S. Treasury and before the start of 2024, there must be at least 40 percent of eligible critical minerals to qualify. Vehicles placed in service in 2024 must have at least 50 percent critical minerals in their batteries. Critical minerals must be 60 percent, 70 percent and 80 percent of a battery’s components in 2025, 2026 and after Dec. 31, 2026, respectively. Dependent on future guidelines developed by the Internal Revenue Service, manufacturers will have to sign off on battery component makeup.

Requirements for Battery Manufacturing/Assembly Requirements

According to Section 30D(e)(2), prior to Jan. 1, 2024, at least half of the components of an EV battery must be assembled or manufactured in North America. Starting in 2024 and through 2025, 60 percent of a battery must meet such requirements. Beginning in 2026 through 2028, this requirement will increase by 10 percent annually, eventually requiring 100 percent of a battery’s construction to meet these standards beyond Dec. 31, 2028.

Other Considerations for Tax Credit Eligibility

If any critical minerals were extracted, handled or recycled by a “foreign entity of concern,” it is prohibited by the IRA for tax credit eligibility. Similarly, final assembly also must take place within North America to retain eligibility for the tax credit. Being considered a “qualified manufacturer” is another requirement that is necessary to maintain tax credit eligibility. This is any manufacturer that adheres to the EPA’s Title II Clean Air Act rules.

With the push for cleaner and greener energy evolving, this is one of many tax credits for consumers and businesses alike to reduce emissions and navigate the U.S. Tax Code.

Electric Vehicle Tax Credits and the Future of the Automotive Industry

September 1, 2022 · Blog, News, Tax and Financial News

⏱ 3 min read

One highlight of the recently passed Inflation Reduction Act of 2022 (IRA; HR 5376) includes modifications to what is more commonly referred to as EV credits. Specifically, Section 30D of the Act is where the most important modifications are, and where the present tax credit for electric vehicles is spelled out in the U.S. Code. There is also new stimulus for previously owned electric vehicles, industrial vehicles and “alternative fuel refueling property.”

According to the Joint Committee on Taxation’s estimates, in lieu of what was previously known as the credit for plug-in electric vehicles, there is now a new clean vehicle credit. It is expected to be worth $7.5 billion over the next decade. Other noteworthy tax credits include $1.7 billion for “alternative fuel refueling property,” $1.3 billion available for buying a previously owned qualified plug-in EV, and $3.6 billion in tax credits for qualified commercial clean vehicles.

How the IRA Changes Section 30D and EV Tax Credits

For eligible, new clean vehicles, purchasers may receive $7,500 in federal tax credits and $4,000 for similarly used vehicles. It is important to note that taxpayers who purchase such vehicles are eligible for this tax credit if their modified adjusted gross income (MAGI) during the current or preceding tax year is no greater than $300,000 for joint filers; $225,000 for heads of household; and $150,000 for single filers. It is also limited to pickup trucks, vans, and sport utility vehicles up to a MSRP of $80,000. All other vehicles costing up to $55,000 are similarly eligible.

Critical Mineral Standards

Another important qualification for this tax credit is if the vehicle’s battery has a minimum threshold of critical minerals and if it has been processed in the required geographies. Section 30D(e) requires progressively increasing percentages of critical minerals either processed or extracted in the United States or another country the U.S. has an existing free-trade agreement with. If the stated percentages are recycled in North America, a vehicle’s battery components may also qualify for the tax credit.

Once guidance is issued by the U.S. Treasury and before the start of 2024, there must be at least 40 percent of eligible critical minerals to qualify. Vehicles placed in service in 2024 must have at least 50 percent critical minerals in their batteries. Critical minerals must be 60 percent, 70 percent and 80 percent of a battery’s components in 2025, 2026 and after Dec. 31, 2026, respectively. Dependent on future guidelines developed by the Internal Revenue Service, manufacturers will have to sign off on battery component makeup.

Requirements for Battery Manufacturing/Assembly Requirements

According to Section 30D(e)(2), prior to Jan. 1, 2024, at least half of the components of an EV battery must be assembled or manufactured in North America. Starting in 2024 and through 2025, 60 percent of a battery must meet such requirements. Beginning in 2026 through 2028, this requirement will increase by 10 percent annually, eventually requiring 100 percent of a battery’s construction to meet these standards beyond Dec. 31, 2028.

Other Considerations for Tax Credit Eligibility

If any critical minerals were extracted, handled or recycled by a “foreign entity of concern,” it is prohibited by the IRA for tax credit eligibility. Similarly, final assembly also must take place within North America to retain eligibility for the tax credit. Being considered a “qualified manufacturer” is another requirement that is necessary to maintain tax credit eligibility. This is any manufacturer that adheres to the EPA’s Title II Clean Air Act rules.

With the push for cleaner and greener energy evolving, this is one of many tax credits for consumers and businesses alike to reduce emissions and navigate the U.S. Tax Code.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

Despite borrowing massive amounts of money, the government still needs to find ways to raise revenue to pay for new programs and spending. The current democratically controlled Congress is looking to potentially implement new social programs and a climate bill. As a way of funding these initiatives, they are considering an expansion of the Net Investment Income Tax (NIIT).

The NIIT is proposed to raise revenue since it is seen as politically more palatable, given that it typically only impacts a small group of wealthier taxpayers. Critics, however, say the plan in its current form would also hurt small family businesses.

Who Pays NIIT Now?

Under the Affordable Care Act (ACA), the NIIT applied a 3.8 percent tax on investment income. Investment income includes both passive sources like dividends, capital gains, interest, royalties, and rents as well as passive business income. Under the ACA, the NIIT applied only to single taxpayers earning $200k or more and joint filers with $250k or more.

When it comes to the taxability of business income under the NIIT, because the law only captures passive business income, most owners of pass-through entities must pay the NIIT; however, active owners of S-corporations are exempt. Likewise, if someone qualifies as a real estate professional, their income is considered active and so their rental income is also exempt.

Who Would Pay Under the New Proposed Law?

The current version of the House bill makes two major changes. First, the NIIT expands to capture all business income. Essentially, S-corporation shareholders, limited partners, and pass-through entity owners that are currently exempt would be impacted.

Second, when it comes to removing the exemption on this business income, the income threshold rises from $200k to $400k for single filers and from $250k to $500k for taxpayers filing jointly. The effect of this would be to exclude most business owners from the tax, but make filing more complex for those impacted.

Under the new rules, the Tax Policy Center projects that in 2023 the tax hike would fall on those in the top 1 percent of household incomes or those making approximately $885k or more. Further, even among the top 1 percent, more than 50 percent of the tax increase would be borne by the top 0.1 percent for those making $4 million and up.

Impact No Small Businesses

Overall, about 14 percent of taxpayers report some form of business income on their federal tax returns. The amount reported, however, is usually not a material amount for most as a percentage of their income. For example, only approximately 5.5 percent of taxpayers with reported business income had this as the source of 50 percent or more of their total income. As a result, the impact will be mostly on a small percentage of small businesses. At the same time, as business income is far more variable than employment income, someone could easily fall in and out of the tax range.

Conclusion

Overall, the House bill looks to raise the threshold of where the NIIT expansion applies by the type of income it captures. We will have to wait and see if there are changes as the bill makes its way through – if it even passes at all. No matter what happens, there will certainly be tax increases of some kind.

Expanding the Net Investment Income Tax

August 1, 2022 · Blog, News, Tax and Financial News

⏱ 3 min read

Despite borrowing massive amounts of money, the government still needs to find ways to raise revenue to pay for new programs and spending. The current democratically controlled Congress is looking to potentially implement new social programs and a climate bill. As a way of funding these initiatives, they are considering an expansion of the Net Investment Income Tax (NIIT).

The NIIT is proposed to raise revenue since it is seen as politically more palatable, given that it typically only impacts a small group of wealthier taxpayers. Critics, however, say the plan in its current form would also hurt small family businesses.

Who Pays NIIT Now?

Under the Affordable Care Act (ACA), the NIIT applied a 3.8 percent tax on investment income. Investment income includes both passive sources like dividends, capital gains, interest, royalties, and rents as well as passive business income. Under the ACA, the NIIT applied only to single taxpayers earning $200k or more and joint filers with $250k or more.

When it comes to the taxability of business income under the NIIT, because the law only captures passive business income, most owners of pass-through entities must pay the NIIT; however, active owners of S-corporations are exempt. Likewise, if someone qualifies as a real estate professional, their income is considered active and so their rental income is also exempt.

Who Would Pay Under the New Proposed Law?

The current version of the House bill makes two major changes. First, the NIIT expands to capture all business income. Essentially, S-corporation shareholders, limited partners, and pass-through entity owners that are currently exempt would be impacted.

Second, when it comes to removing the exemption on this business income, the income threshold rises from $200k to $400k for single filers and from $250k to $500k for taxpayers filing jointly. The effect of this would be to exclude most business owners from the tax, but make filing more complex for those impacted.

Under the new rules, the Tax Policy Center projects that in 2023 the tax hike would fall on those in the top 1 percent of household incomes or those making approximately $885k or more. Further, even among the top 1 percent, more than 50 percent of the tax increase would be borne by the top 0.1 percent for those making $4 million and up.

Impact No Small Businesses

Overall, about 14 percent of taxpayers report some form of business income on their federal tax returns. The amount reported, however, is usually not a material amount for most as a percentage of their income. For example, only approximately 5.5 percent of taxpayers with reported business income had this as the source of 50 percent or more of their total income. As a result, the impact will be mostly on a small percentage of small businesses. At the same time, as business income is far more variable than employment income, someone could easily fall in and out of the tax range.

Conclusion

Overall, the House bill looks to raise the threshold of where the NIIT expansion applies by the type of income it captures. We will have to wait and see if there are changes as the bill makes its way through – if it even passes at all. No matter what happens, there will certainly be tax increases of some kind.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into the heart of taxpayers. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

Decline in Audit Rates

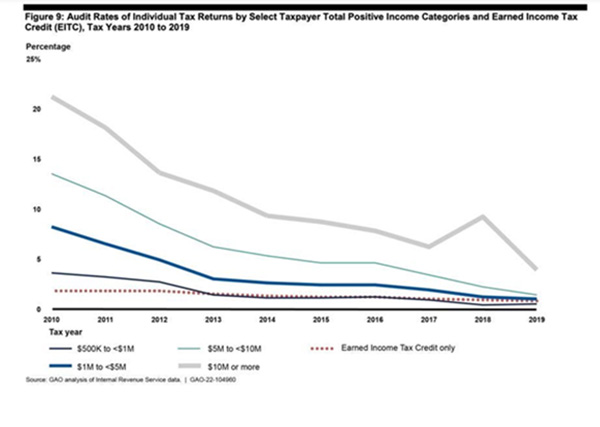

The rate at which the IRS is auditing individual taxpayers has declined overall between the years of 2010 and 2019 (2020 data is too new and 2021 returns are still being filed through the extension period). According to the Government Accountability Office (GAO), nearly 1 percent of all taxpayers were audited in 2010 compared to only 0.25 percent for the tax year 2019. The GAO chart below shows the ski slope-like drop in individual tax audit rates over the period.

While the IRS continues to audit higher earning taxpayers more often overall, during the 10-year period audit rates consistently declined for all levels of taxpayers, except those with the highest incomes. The audit rate for taxpayers with income between $200k and $500k experienced the largest drop, with the audit rate declining from 2.3 percent down to 0.2 percent; a 92 percent reduction in audits. Taxpayers with the highest incomes, defined as $10 million or more, saw a resurgence in audit rates from 2017-2018; however, even they experienced an overall decline, dropping from 21.2 percent in 2019 to only 3.9 percent in 2019 – equating to an 81 percent decline.

Impact on the Treasury

There is the theory that the prospect of a tax audit leads to greater voluntary compliance. In other words, if people think they won’t get audited, then they are more likely to cheat on their taxes.

Non-compliance with tax laws and regulations have a material impact on the Treasury. According to the IRS, it is estimated that on average, individual taxpayers under-reported nearly $250 billion a year for the period 2011-2013. This obviously leads to the non-collection of taxes that are otherwise owed the government and raises issues of fairness for taxpayers who are playing by the rules.

Why the Decline in Audit Rates?

One of the main drivers is a lack of resources at the IRS, a combination of both reduced funding and less auditors on staff. The number of agents working for the IRS has declined across the board since 2011. Tax examiners, the type who handle basic audits by mail, have dropped by 18 percent. Meanwhile, revenue agents, who handle the more complex cases in the field, declined by more than 40 percent over the same period.

Demographics point to an increase in these trends as there are a wave of coming retirements in the IRS. Over the next three years, nearly 14 percent of current tax examiners and 16 percent of revenue agents are expected to retire. Stack on top of this the fact that the inexperience of newer agents and the time to complete audits is also taking longer.

Conclusion

The IRS claims it is missing out on millions in legally due tax revenues due to the inability to maintain enforcement. They say they need more funding to hire more agents to perform more audits, which not only find fraud in the audits themselves but also increase overall compliance due to the pressure this creates.

Currently, there is no political focus on bringing major new resources to the IRS, so it’s not likely to see an uptick in individual tax audit rates anytime soon. The trend of focusing on the highest earners, however, will likely continue as this is where the IRS can find the most bang for its buck.

The IRS is Auditing Fewer Returns than Ever

July 1, 2022 · Blog, News, Tax and Financial News

⏱ 3 min read

One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into the heart of taxpayers. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

Decline in Audit Rates

The rate at which the IRS is auditing individual taxpayers has declined overall between the years of 2010 and 2019 (2020 data is too new and 2021 returns are still being filed through the extension period). According to the Government Accountability Office (GAO), nearly 1 percent of all taxpayers were audited in 2010 compared to only 0.25 percent for the tax year 2019. The GAO chart below shows the ski slope-like drop in individual tax audit rates over the period.

While the IRS continues to audit higher earning taxpayers more often overall, during the 10-year period audit rates consistently declined for all levels of taxpayers, except those with the highest incomes. The audit rate for taxpayers with income between $200k and $500k experienced the largest drop, with the audit rate declining from 2.3 percent down to 0.2 percent; a 92 percent reduction in audits. Taxpayers with the highest incomes, defined as $10 million or more, saw a resurgence in audit rates from 2017-2018; however, even they experienced an overall decline, dropping from 21.2 percent in 2019 to only 3.9 percent in 2019 – equating to an 81 percent decline.

Impact on the Treasury

There is the theory that the prospect of a tax audit leads to greater voluntary compliance. In other words, if people think they won’t get audited, then they are more likely to cheat on their taxes.

Non-compliance with tax laws and regulations have a material impact on the Treasury. According to the IRS, it is estimated that on average, individual taxpayers under-reported nearly $250 billion a year for the period 2011-2013. This obviously leads to the non-collection of taxes that are otherwise owed the government and raises issues of fairness for taxpayers who are playing by the rules.

Why the Decline in Audit Rates?

One of the main drivers is a lack of resources at the IRS, a combination of both reduced funding and less auditors on staff. The number of agents working for the IRS has declined across the board since 2011. Tax examiners, the type who handle basic audits by mail, have dropped by 18 percent. Meanwhile, revenue agents, who handle the more complex cases in the field, declined by more than 40 percent over the same period.

Demographics point to an increase in these trends as there are a wave of coming retirements in the IRS. Over the next three years, nearly 14 percent of current tax examiners and 16 percent of revenue agents are expected to retire. Stack on top of this the fact that the inexperience of newer agents and the time to complete audits is also taking longer.

Conclusion

The IRS claims it is missing out on millions in legally due tax revenues due to the inability to maintain enforcement. They say they need more funding to hire more agents to perform more audits, which not only find fraud in the audits themselves but also increase overall compliance due to the pressure this creates.

Currently, there is no political focus on bringing major new resources to the IRS, so it’s not likely to see an uptick in individual tax audit rates anytime soon. The trend of focusing on the highest earners, however, will likely continue as this is where the IRS can find the most bang for its buck.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

COVID-19 impacted the economy dramatically and commercial real estate was no exception in terms of decreased values. Often, the real property could no longer service the debt used to finance it. This debt restructuring and resulting debt forgiveness can result in taxable income.

Taxable Income and Debt Cancellation

If you have a $80,000 loan and the bank reduced the amount you owe down to $50,000, then you have an economic benefit of $30,000, which should be treated as taxable income. This is indeed how cancellation of debt is treated, but there are exceptions such as in the case of bankruptcy or insolvency. There is another unique scenario that applies only to commercial real estate.

Assuming that the taxpayer is not a C-corporation, debt cancellation is excludable from taxable income if it results from qualified real property business indebtedness (QRPBI). QRPBI is debt taken on to buy real property used for commercial purposes. Starting in 1993, debt used for building or improving a property also qualify.

As we all know, there is no such thing as a free lunch. In order for debt cancellation to not be considered current taxable income, the taxpayer must reduce their basis in the real property by this same amount. This does not cancel the income; instead, it defers its recognition and helps cash flow as a result. Below, we look at an example of how this works.

Illustrative Example

Assume David bought a property in 2017 and he uses it for business purposes. In 2022, the property has a first mortgage of $200,000 and a second mortgage of $100,000 (both with the same bank), with a fair market value (FMV) of $240,000. He negotiates with the bank to reduce the second mortgage down to $20,000, resulting in income from the cancellation of debt of $80,000.

The amount of debt cancellation that can be deferred is equal to the amount of the second mortgage before the debt cancellation, less the FMV minus the first mortgage. In David’s case, before debt cancellation, the FMV ($240k) minus the first mortgage ($200k) was $40,000. The balance of the second mortgage ($100k) exceeded this by $60,000. Out of the total debt cancellation of $80,000, this $60k is subject to deferral, with only the remaining $20,000 reported as immediate taxable income.

The $60,000 is not considered as taxable income only to the extent that David has sufficient adjusted tax basis in the depreciable real property to absorb this as a reduction in basis. Assuming this is the case, the reduction in basis applies the first day of the tax year after the debt cancellation (unless the property is sold before year-end – then it applies immediately).

In the example above, David would include the $10,000 of cancellation of debt income on his 2022 tax return and adjust his basis in the real property by $60,000 as of Jan. 1, 2023.

Filing Mechanics

For real estate held via partnerships instead of by individuals, determining if debt is QRPBI qualified happens at the entity level, although reductions of basis are done at the individual level for each partner, allowing individual planning. The election to defer cancellation of debt income is recorded on Form 982.

Conclusion

The COVID pandemic caused many real estate investors to restructure their debts. The option to defer debt income cancellation offers a great tax planning opportunity by delaying taxable income and improving cash flows.

Tax Break for Commercial Real Estate Investors

June 1, 2022 · Blog, News, Tax and Financial News

⏱ 3 min read

COVID-19 impacted the economy dramatically and commercial real estate was no exception in terms of decreased values. Often, the real property could no longer service the debt used to finance it. This debt restructuring and resulting debt forgiveness can result in taxable income.

Taxable Income and Debt Cancellation

If you have a $80,000 loan and the bank reduced the amount you owe down to $50,000, then you have an economic benefit of $30,000, which should be treated as taxable income. This is indeed how cancellation of debt is treated, but there are exceptions such as in the case of bankruptcy or insolvency. There is another unique scenario that applies only to commercial real estate.

Assuming that the taxpayer is not a C-corporation, debt cancellation is excludable from taxable income if it results from qualified real property business indebtedness (QRPBI). QRPBI is debt taken on to buy real property used for commercial purposes. Starting in 1993, debt used for building or improving a property also qualify.

As we all know, there is no such thing as a free lunch. In order for debt cancellation to not be considered current taxable income, the taxpayer must reduce their basis in the real property by this same amount. This does not cancel the income; instead, it defers its recognition and helps cash flow as a result. Below, we look at an example of how this works.

Illustrative Example

Assume David bought a property in 2017 and he uses it for business purposes. In 2022, the property has a first mortgage of $200,000 and a second mortgage of $100,000 (both with the same bank), with a fair market value (FMV) of $240,000. He negotiates with the bank to reduce the second mortgage down to $20,000, resulting in income from the cancellation of debt of $80,000.

The amount of debt cancellation that can be deferred is equal to the amount of the second mortgage before the debt cancellation, less the FMV minus the first mortgage. In David’s case, before debt cancellation, the FMV ($240k) minus the first mortgage ($200k) was $40,000. The balance of the second mortgage ($100k) exceeded this by $60,000. Out of the total debt cancellation of $80,000, this $60k is subject to deferral, with only the remaining $20,000 reported as immediate taxable income.

The $60,000 is not considered as taxable income only to the extent that David has sufficient adjusted tax basis in the depreciable real property to absorb this as a reduction in basis. Assuming this is the case, the reduction in basis applies the first day of the tax year after the debt cancellation (unless the property is sold before year-end – then it applies immediately).

In the example above, David would include the $10,000 of cancellation of debt income on his 2022 tax return and adjust his basis in the real property by $60,000 as of Jan. 1, 2023.

Filing Mechanics

For real estate held via partnerships instead of by individuals, determining if debt is QRPBI qualified happens at the entity level, although reductions of basis are done at the individual level for each partner, allowing individual planning. The election to defer cancellation of debt income is recorded on Form 982.

Conclusion

The COVID pandemic caused many real estate investors to restructure their debts. The option to defer debt income cancellation offers a great tax planning opportunity by delaying taxable income and improving cash flows.

Disclaimer

These articles are intended to provide general resources for the tax and accounting needs of small businesses and individuals. Service2Client LLC is the author, but is not engaged in rendering specific legal, accounting, financial or professional advice. Service2Client LLC makes no representation that the recommendations of Service2Client LLC will achieve any result. The NSAD has not reviewed any of the Service2Client LLC content. Readers are encouraged to contact a professional regarding the topics in these articles. The images linked to these articles are protected by copyright and should not be copied for any reason.

At the very end of March, the House of Representatives passed a version of the bill known as Secure 2.0. The bill passed the House with overwhelming bipartisan support in a 414-5 vote. The House version still needs to pass in the Senate, where there are differing ideas on exactly what the bill should contain. There is strong support, so it is less of a question of if Secure 2.0 will become law than what exact version.

The Secure 2.0 bill in any version aims to help Americans save for retirement through a variety of mechanisms and changes in tax law. Here are some highlights of what the bill hopes to accomplish and how. We’ll also note differences between the House and Senate plans throughout.

Sign Up More Workers for Retirement Plans

One way the House version of the bill aims to help people save for retirement is to simply get them into a plan. The law would automatically enroll workers in 401(k), 403(b) and SIMPLE IRA retirement plans in their workplace; however, they can opt out. It’s been shown that most people simply won’t take action, meaning they won’t enroll if they have to proactively sign up – and similarly won’t opt out. The Senate version does not require auto enrollment, but it does give companies incentives to structure plans so that they auto enroll workers.

Auto enrollment in the House version starts at three percent contributions and increases yearly until participants are contributing 10 percent of their pay. Business with 10 or fewer employees are exempt.

Encourage Small Employers

Workplace retirement plans come with administrative, financial and legal burdens just to set up and offer the plan. This is before any type of employer contributions and is often a roadblock to small employers offering plans to their employees. To help encourage small employers, the bill offers a retirement plan start-up tax credit of 100 percent for the first three years to cover these costs.

Bigger Catch-Up Contributions

Right now, 401(k) plan catch-up contributions for workers 50 and older are capped at $6,500 for 401(k) plans. Both the House and Senate versions offer to increase these amounts, but in different ways.

The House version increases 401(k) catch-up contributions up to $10,000 for those 62, 63 or 64 starting in 2024. A more generous version is offered by the Senate, allowing the same $10,000 limit but to all who are 60 or older.

There is a “catch” to the catch-up, however. Under both versions, all catch-up contributions to 401(k) plans will be treated as Roth contributions; i.e., after tax contributions beginning in 2023. Currently, workers can make the contributions on either a pre-tax or post-tax (Roth) basis.

Push-Out Mandatory Required Distributions

The House version would extend the age for taking required minimum distributions (RMD) from retirements plans from 72 up to 75, incrementally over 3 years (73 in 2023, 74 in 2030 and 75 in 2033).

The Senate plan raises the age to 75 by 2032 and also waives RMDs entirely for those with less than $100,000 in aggregate retirement savings. It also reduces the penalty for not taking RMDs down to 25 percent (currently 50 percent).

Expand Employer Matching

The way the vast majority of retirement plans work is that employees contribute a portion of their salary and then the employer contributes a matching amount of 50 percent or 100 percent of what employee saves (up to a limit). The Secure 2.0 bill proposes to make student loan payments qualify as deferrals the same as plan contributions. This means that if you make student loan payments, your employer can now make a matching contribution to your retirement plan account even though you are not actually making any contributions into the plan itself. This is not a requirement, but an option for employers.

Create a Lost and Found for Retirement Plans

It’s common for workers to lose track of retirement plans from previous jobs when they move and change jobs. The bill would create a national lost and found to aid people in locating plans they may have inadvertently left behind or forgotten about.

Conclusion

In whatever form the final bill takes shape, it will give Americans more options to save for retirement and expand access to workplace plans.

Secure 2.0 Retirement Bill

May 1, 2022 · Blog, News, Tax and Financial News

⏱ 4 min read

At the very end of March, the House of Representatives passed a version of the bill known as Secure 2.0. The bill passed the House with overwhelming bipartisan support in a 414-5 vote. The House version still needs to pass in the Senate, where there are differing ideas on exactly what the bill should contain. There is strong support, so it is less of a question of if Secure 2.0 will become law than what exact version.

The Secure 2.0 bill in any version aims to help Americans save for retirement through a variety of mechanisms and changes in tax law. Here are some highlights of what the bill hopes to accomplish and how. We’ll also note differences between the House and Senate plans throughout.

Sign Up More Workers for Retirement Plans